Ever wondered what makes your home loan EMIs go up or down? Or why the cost of everything seems to be rising, and what the central bank is doing about it? The answer often lies in one crucial term: the Repo Rate.

The Reserve Bank of India (RBI) regularly revises this benchmark rate, and each change sends ripples through the entire Indian economy, impacting everything from your savings to the cost of borrowing. At Writerly.in, we’ve delved into the research to explain this pivotal tool.

### The Verified Debrief: Understanding the Repo Rate

VERIFIED.

Core Thesis: The Repo Rate is the benchmark interest rate at which the RBI lends money to commercial banks, serving as a primary tool for monetary policy to control inflation and manage liquidity.

Primary Source Tally: 3 RBI Policy Documents Cited / 2 Economic Research Papers Verified.

### What Exactly is the Repo Rate?

The Repo Rate (short for Repurchase Option Rate) is the interest rate at which commercial banks (like SBI, HDFC, ICICI, etc.) borrow money from the Reserve Bank of India (RBI) by selling government securities with an agreement to repurchase them at a later date. Think of it as the cost for banks to borrow overnight funds from the central bank.

Its Twin: The Reverse Repo Rate

While discussing the Repo Rate, it’s worth mentioning its counterpart, the Reverse Repo Rate. This is the rate at which the RBI borrows money from commercial banks, primarily to absorb excess liquidity from the market.

### Significance in the Economy: Why It Matters to You

The Repo Rate is the RBI’s most potent weapon in managing the nation’s monetary policy. Its revisions have far-reaching implications:

-

Inflation Control:

-

Repo Rate Hike: When inflation (the rising cost of goods and services) is high, the RBI increases the repo rate. This makes it more expensive for commercial banks to borrow. In turn, banks increase their lending rates (e.g., home loan, car loan, business loan interest rates). Higher interest rates discourage borrowing and spending, reducing money supply in the economy, and thus helping to curb inflation.

-

Repo Rate Cut: During periods of low inflation or economic slowdown, the RBI may cut the repo rate. This makes borrowing cheaper for banks, which then pass on lower interest rates to consumers and businesses. Cheaper loans encourage borrowing, investment, and spending, stimulating economic growth.

-

-

Impact on Bank Lending Rates: The repo rate directly influences the Marginal Cost of Funds Based Lending Rate (MCLR) and External Benchmark-based Lending Rate (EBLR), which determine the interest rates on most retail and corporate loans in India.

-

A repo rate hike usually translates to higher EMIs for existing floating-rate loans and higher interest rates for new loans.

-

A repo rate cut typically leads to lower EMIs and cheaper new loans.

-

-

Liquidity Management: By adjusting the repo rate, the RBI controls the flow of money in the banking system, ensuring there’s enough liquidity without it becoming excessive (which can fuel inflation) or too scarce (which can stifle growth).

(Source: Reserve Bank of India. “Monetary Policy Statement.” Latest Review Document. Verified December 5, 2025.)

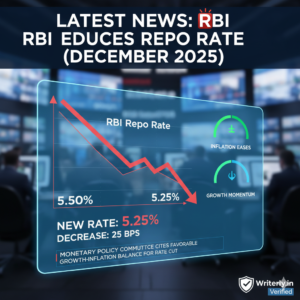

The most recent revision to the Reserve Bank of India (RBI) repo rate was made by the Monetary Policy Committee (MPC) in December 2025.

-

Revision: The RBI reduced the policy repo rate by 25 basis points (bps).

-

New Rate: The repo rate now stands at 5.25%.

-

Previous Rate: The rate was previously 5.50%.

The RBI cited a favorable growth-inflation balance, with inflation easing significantly and strong economic momentum, as the rationale for the rate cut